TSP to Gold IRA Guide: Convert Thrift Savings Plan to Gold

While a TSP cannot hold gold directly, federal employees and military personnel can invest in physical gold through a TSP rollover to a Gold IRA. A self-directed Gold IRA (Gold SDIRA) allows for investment in IRA-approved precious metals such as gold, silver, platinum, and palladium.

Before starting a TSP rollover to a Gold IRA, understand its eligibility, tax implications, benefits, steps, best companies, and costs you will face during this process. Focus on the User covers everything you need to know about this rollover process for TSPs below.

- To convert your TSP account to a Gold IRA, you must first work with a Gold IRA company and custodian to help you through the process.

- A TSP cannot hold gold but can be rolled over into a Gold IRA to hold gold bullion coins and bars.

- A Thrift Savings Plan (TSP) is a retirement and investment plan offered to federal government employees and members of the uniformed services.

What is a Gold TSP Rollover?

A Gold TSP Rollover allows federal employees and military personnel to transfer their Thrift Savings Plan (TSP) retirement funds into a Gold IRA, enabling them to invest in physical gold such as gold bars or coins.

This rollover can be done through a direct transfer, where funds move directly from the TSP to the Gold IRA custodian, or an indirect transfer, where the account holder receives the funds and deposits them into the Gold IRA within 60 days.

Eligibility

To be eligible for a TSP to Gold IRA rollover, you generally need to have separated from federal service, be retired, or have reached the age of 59 ½. Active federal employees or military personnel may not be eligible unless they qualify for an exception. The IRS and TSP administrators regulate eligibility based on employment status, and those who meet these conditions can move their TSP funds into a Gold IRA to diversify their retirement portfolio.

Tax Implications

A direct rollover from a TSP to a Gold IRA is tax-deferred, meaning no immediate taxes or penalties are incurred. However, if an indirect rollover is chosen, the funds must be deposited into the new Gold IRA within 60 days to avoid income taxes and a potential 10% early withdrawal penalty for those under 59 ½. The IRS requires reporting of the rollover using Form 1099-R, ensuring the process remains compliant with their tax rules.

Benefits of Rolling Over Your TSP to a Gold IRA

Diversifying your TSP into precious metals such as gold offers many benefits to keeping your savings safe and secure.

- Hedge Against Inflation: Gold offers protection from inflation as its value tends to rise when the dollar weakens.

- Diversification: A Gold IRA diversifies your portfolio with physical assets, reducing reliance on paper-based investments.

- Tangible Asset: Unlike stocks or bonds, gold is a physical asset that retains intrinsic value.

- Wealth Preservation: Gold helps preserve wealth over time, especially during market downturns or economic uncertainty.

- Tax Advantages: A Gold IRA rollover maintains tax-deferred growth, just like your TSP.

- Control Over Investments: With a self-directed Gold IRA, you gain more control over your investment choices, such as selecting specific gold products.

See all pros and cons of Gold IRAs, understand exactly what makes these IRAs so unique.

TSP vs Gold IRA

| TSP | Gold IRA | |

|---|---|---|

| Investment Type | Primarily paper assets (stocks, bonds) | Physical assets (gold, silver, etc.) |

| Inflation Protection | Limited, tied to market performance | Strong protection against inflation |

| Diversification | Limited to paper assets | Diversifies with precious metals |

| Control Over Investments | Limited to TSP fund options | Full control over specific gold investments |

| Can Hold Gold | No | Yes |

How to Roll Over Your TSP to a Gold IRA

The steps involved in converting your TSP to a Gold IRA are straight forward on the surface, but it is important you thoroughly understand this process. A Gold IRA company will also help you through the Gold IRA rollover. Below is what you can expect:

- Check Eligibility: Confirm that your TSP account is eligible for rollover into a Gold IRA, typically after leaving federal employment or reaching a certain age.

- Select a Gold IRA Company: Choose a reputable Gold IRA provider that specializes in handling TSP rollovers and offers secure storage options.

- Open a Gold IRA: Set up your new self-directed Gold IRA account with the chosen provider to receive the rolled-over funds.

- Initiate the TSP Rollover Process: Contact your TSP administrator to request a rollover of funds into your newly opened Gold IRA.

- Choose Gold Assets: Work with your Gold IRA provider to select eligible gold products, such as bullion or coins, that meet IRS requirements.

- Buy Gold For New Gold IRA: Complete the purchase of selected gold assets, which are then transferred to your Gold IRA and stored securely.

Fees

When rolling over your TSP to a Gold IRA, there are various fees to consider, ranging from setup to storage costs. Below you can review the typical costs of fees you can expect.

| Fee Type | Range | Details |

|---|---|---|

| Setup Fees | $50 to $300 | Covers the initial account creation. |

| Annual Maintenance Fees | $80 to $300 per year | Charged for ongoing account management. |

| Storage Fees | $100 to $500+ per year | Ensures secure storage for your gold, either segregated or non-segregated. |

| Transfer/Rollover Fees | $25 to $260 | Incurred when moving your TSP funds to a Gold IRA. |

Fees can vary depending on your chosen Gold IRA provider, the type of storage, and the level of service, so it's important to compare options to find the best fit. We cover all fees in a Gold IRA so you can prepare before you roll over your TSP.

Common Mistakes to Avoid During TSP to Gold IRA

When rolling over your TSP to a Gold IRA, it’s essential to understand potential mistakes that could lead to taxes, penalties, or mismanagement of your retirement savings. Below are the most common mistakes you must avoid during the rollover process:

- Failing to do a direct rollover, which can lead to taxes and penalties.

- Choosing a non-IRS-approved custodian or trustee for your Gold IRA.

- Not meeting IRS gold purity requirements (99.5% for gold).

- Missing the 60-day rollover deadline if doing an indirect rollover.

- Overlooking fees, such as setup, storage, and maintenance costs.

- Not diversifying by moving all TSP funds into gold without considering other assets.

- Ignoring IRS contribution and distribution rules, including Required Minimum Distributions (RMDs).

It is important to consult with a licensed financial advisor to avoid any of these mistakes when rolling over your TSP. Gold IRA companies can help you through these complicated processes to avoid penalties.

Storage Requirements

When rolling over your TSP to a Gold IRA, you must store your physical gold in an IRS-approved storage facility. There are two main storage options: Segregated (Allocated) Storage and Non-Segregated (Commingled) Storage, each with its own costs and benefits.

Segregated Storage (Allocated Storage)

Your gold is stored separately from other investors' assets in a dedicated space. This option ensures that the exact gold you purchase is the gold you’ll receive when you liquidate. It offers the highest level of security and privacy, with fees ranging from $100 to $300+ per year.

Non-Segregated Storage (Commingled Storage)

Your gold is stored alongside other investors' assets in a shared space. While more cost-effective, with fees ranging from $50 to $150+ per year, you may not receive the exact bars or coins you originally purchased upon liquidation, though their value remains the same.

The choice between segregated and non-segregated storage often depends on the level of security you desire and the amount you’re investing. Larger investments may benefit from segregated storage, while smaller portfolios could opt for the lower-cost non-segregated option. Work with your Gold IRA custodian to see what storage options they provide to ensure you get the best Gold IRA storage option that best aligns with your TSP.

IRA-Approved Gold for Your New Gold IRA

It's important to consider the IRA-approved gold you are allowed to include in your new Gold IRA after you convert your TSP. Not all gold is allowed, make sure you invest in only IRA-approved precious metals.

American Eagle Gold Coins

Mint:

U.S. Mint

Purity:

91.67% (22-karat)

Denominations:

1 oz, 1/2 oz, 1/4 oz, 1/10 oz

Key Features:

Iconic design, most popular Gold IRA coin, recognized worldwide.

Canadian Maple Leaf Gold Coins

Mint:

Royal Canadian Mint

Purity:

99.99% (24-karat)

Denominations:

1 oz, 1/2 oz, 1/4 oz, 1/10 oz, 1/20 oz

Key Features:

Known for purity and security features, widely accepted.

Austrian Philharmonic Gold Coins

Mint:

Austrian Mint

Purity:

99.99% (24-karat)

Denominations:

1 oz, 1/2 oz, 1/4 oz, 1/10 oz

Key Features:

Europe's best-selling gold coin, recognized worldwide.

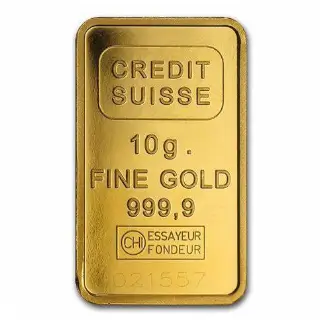

Credit Suisse Gold Bars

Manufacturer:

Credit Suisse

Purity:

99.99% (.9999)

Sizes:

1 gram to 1 kg

Key Features:

Widely accepted, serial numbered, highly reputable.

Choose a Gold IRA Company For Your TSP Rollover

Comparing the industry-leading TSP to Gold IRA companies with the best reputations across the board. Focus on the User reviewed all of the leading companies so you can easily find one perfect for your TSP rollover to gold.

TSP Rollover FAQ

Yes, TSP participants can roll over eligible rollover distributions to a qualified trust or an eligible retirement plan, such as an IRA or an eligible employer plan, as defined in IRS code IRC § 402(c)(8)). (5 USC § 8433(c)(2).

A Gold TSP rollover is not taxed as long as the rollover is performed correctly, such as through a direct rollover, which ensures that funds are transferred directly from the TSP to the Gold IRA without any penalties or tax implications.

Yes, you can roll over a portion of your TSP balance into a Gold IRA. This allows you to diversify your investments while keeping part of your balance in traditional assets. You can even diversify your TSP further into a Silver IRA rollover to hold more than one type of metal.

Required documents typically include the TSP withdrawal form, Gold IRA account details from your custodian, and any necessary identification or financial verification forms.

Only gold that meets IRS requirements can be invested in, such as gold with a purity of at least 99.5%. This includes IRA-approved coins and bars like the American Gold Eagle and Canadian Maple Leaf.

The TSP rollover process typically takes 2 to 4 weeks, depending on how quickly the TSP processes your distribution and how efficiently the Gold IRA custodian sets up your account.

A TSP rollover involves moving funds from a TSP to a Gold IRA, usually by direct rollover to avoid taxes. A transfer generally refers to moving funds between two IRAs without taking possession of the funds.

Choose a custodian that is IRS-approved, has a strong reputation, offers good customer service, and has transparent fees for managing and storing your gold.

A good trustee should have experience with self-directed IRAs, be IRS-approved, and provide secure storage options for your physical gold.

No, TSP participants cannot directly invest in gold, gold stocks, or gold exchange-traded funds (ETFs) through their TSP accounts.

How Focus on the User Helps You Convert Your TSP to a Gold IRA

At Focus on the User, we provide the tools and guidance you need to smoothly convert your TSP to a Gold IRA. With expert tips, rollover steps, and resources on tax and storage options, we’re here to help you make informed decisions for securing your retirement with gold. Learn more in our free Gold IRA Guide.