403(b) Rollover to Gold & Silver: How to Convert a 403(b)

to Gold IRA")

Although a 403(b) cannot directly hold gold, employees of public schools, non-profits, and certain government entities can convert their 403(b) to a Self-Directed Gold IRA. This process allows you to diversify retirement holdings in physical gold and other precious metals.

Before converting a 403(b) to a Gold IRA, understand its eligibility, tax implications, benefits, steps, and the costs you will face during this process. Focus on the User covers everything you need to know about this process in our 403(b) to gold guide below.

- To convert your 403(b) to a Gold IRA, work with a specialized Gold IRA company to initiate the rollover and set up a Self-Directed IRA to hold the gold.

- 403(b) accounts are limited to traditional investments but can be rolled over into a Gold IRA to hold IRS-approved gold products.

- A 403(b) is a retirement plan offered to public sector employees, non-profits, and certain ministers.

Rollover")

What is a Gold 403(b) Rollover?

A Gold 403(b) Rollover allows individuals with a 403(b) retirement plan to move their funds into a Gold IRA, a Self-Directed IRA that holds IRS-approved precious metals like gold. This rollover with a Tax-sheltered annuity (TSA) into a Gold IRA, also known as a 403(b), is typically done to diversify retirement savings in alternative physical assets.

There are two methods for the rollover: a Direct Rollover, where funds are transferred directly between the 403(b) and the Gold IRA custodian, and an Indirect Rollover, where the individual temporarily holds the funds and must reinvest them in the Gold IRA within 60 days to avoid taxes and penalties. This process must follow strict IRS regulations to ensure the rollover remains tax-deferred.

Eligibility

To be eligible to rollover your 403(b) to gold, certain criteria must be met. Generally, eligibility requires the individual to have either separated from service (e.g., retired or left their employer) or to have reached the age of 59 ½. At this point, they can move funds from their 403(b) into a Gold IRA without incurring penalties.

Tax Implications

A Gold 403(b) Rollover is typically a tax-deferred transaction, meaning no immediate taxes are owed if the rollover is handled correctly. In a Direct Rollover, the funds go straight from the 403(b) to the Gold IRA custodian, maintaining tax-deferred status. If an Indirect Rollover is used, the funds must be reinvested in the Gold IRA within 60 days to avoid taxes and potential early withdrawal penalties if under 59 ½.

Benefits of Rolling Over Your 403(b) to a Gold IRA

There are some benefits when you roll over a 403(b) into a Self-Directed Gold IRA or other assets.

- Diversify 403(b) Funds: A Gold IRA, using 403(b) funds, can allow investors an additional way to diversify a portfolio.

- Better Control: With a Self-Directed IRA in gold, you'll have more control over which products you want to invest in.

- Can Include Multiple Metals: Other than gold, silver, platinum, and palladium can be held in a Gold IRA from your 403(b) funds.

- Rollover Options: A 403(b) is eligible for a rollover, allowing for a straightforward method of moving funds.

See all pros and cons of Gold IRAs, understand exactly what makes these IRAs unique.

403(b) vs Gold IRA

| 403(b) | Gold IRA | |

|---|---|---|

| Investment Type | Stocks, bonds, annuities | Physical gold and other precious metals |

| Diversification | Paper-based investments | Tangible asset options |

| Control Over Investments | Limited to employer plan options | High, with the ability to select specific gold products |

| Can Hold Gold | No | Yes |

How to Roll Over Your 403(b) to a Gold IRA

Converting a 403(b) to a Gold IRA involves several key steps. A Gold IRA company can assist you throughout the process:

- Check Eligibility: Verify whether your 403(b) account is eligible for rollover, usually upon reaching retirement age or changing employers.

- Select a Gold IRA Company: Choose a reputable Gold IRA provider experienced in handling 403(b) rollovers.

- Open a Gold IRA: Establish a new Self-Directed Gold IRA account with the selected provider to receive the rollover funds.

- Initiate the 403(b) Rollover: Contact your 403(b) plan administrator to arrange the rollover of funds into the new Gold IRA.

- Choose Gold Assets: Work with the Gold IRA provider to select IRS-approved gold coins or bars.

- Buy Gold For New Gold IRA: Complete the purchase of chosen gold assets, which are then transferred and securely stored in your Gold IRA.

The rollover process isn't as compelx as you may think at first. It is very similar to Gold IRA rollovers, as long as you work with an accredited Gold IRA company.

Fees

When rolling over your 403(b) to a Gold IRA, you may encounter several fees, including setup fees, annual maintenance fees, storage fees, and transfer or rollover fees. The expected costs are listed below, giving you a clear view of typical expenses for the process.

| Fee Type | Range | Details |

|---|---|---|

| Setup Fees | $50 to $300 | Covers the initial account creation. |

| Annual Maintenance Fees | $80 to $300 per year | Charged for ongoing account management. |

| Storage Fees | $100 to $500+ per year | Ensures secure storage for your gold, either segregated or non-segregated. |

| Transfer/Rollover Fees | $25 to $260 | Incurred when moving your 403(b) funds to a Gold IRA. |

Fees can vary depending on the Gold IRA firm, the type of account, storage, and service level. We feature all the fees you can expect in a complete list.

Common Mistakes to Avoid During 403(b) to Gold IRA Rollover

Rolling over your 403(b) to a Gold IRA can be beneficial, but it's important to be aware of potential mistakes that could lead to taxes, penalties, or mismanagement of your retirement funds. Here are some key mistakes to avoid:

- Not choosing a direct rollover, which may result in taxes and penalties.

- Using a custodian or trustee that isn't IRS-approved for Gold IRAs.

- Failing to meet IRS purity standards for gold (99.5% purity required).

- Missing the 60-day window to complete an indirect rollover, which can cause tax issues.

- Neglecting to account for fees, including setup, storage, and annual maintenance fees.

- Not diversifying your assets, moving all funds into gold without considering other options.

- Disregarding IRS rules for contributions, distributions, and Required Minimum Distributions (RMDs).

To avoid these issues, it’s essential to work with a reputable Gold IRA company and seek advice from a licensed financial advisor to ensure a smooth 403(b) rollover process.

Storage Requirements

When rolling over your 403(b) to a Gold IRA, IRS rules require that physical gold be stored in an approved facility. You can choose between Segregated (Allocated) Storage and Non-Segregated (Commingled) Storage, each offering different costs and levels of security.

Segregated Storage (Allocated Storage)

In Segregated Storage, your gold is kept separate from other investors' assets. This ensures you receive the exact gold you purchased when liquidating, providing maximum security and privacy. Annual fees for this option typically range from $100 to $300+.

Non-Segregated Storage (Commingled Storage)

Non-Segregated Storage stores your gold alongside assets from other investors. It’s a cost-effective option, with fees typically ranging from $50 to $150+ per year. Although you may not get back the same exact gold pieces, their value remains the same.

The choice between these storage options depends on your security preferences and investment size. Discuss available storage choices with your Gold IRA company to find the right Gold IRA storage option for your 403(b) rollover.

IRA-Approved Precious Metals for New Gold IRA

Once you've rolled over your 403(b) funds to a Gold IRA, invest in only IRA-approved gold and silver as not all precious metals are allowed.

American Eagle Gold Coins

Mint:

U.S. Mint

Purity:

91.67% (22-karat)

Key Features:

Iconic design, most popular Gold IRA coin, recognized worldwide.

Canadian Maple Leaf Gold Coins

Mint:

Royal Canadian Mint

Purity:

99.99% (24-karat)

Key Features:

Known for purity and security features, widely accepted.

Austrian Philharmonic Gold Coins

Mint:

Austrian Mint

Purity:

99.99% (24-karat)

Key Features:

Europe's best-selling gold coin, recognized worldwide.

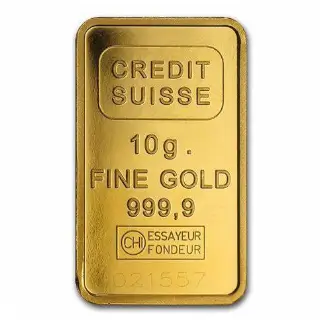

Credit Suisse Gold Bars

Manufacturer:

Credit Suisse

Purity:

99.99% (.9999)

Key Features:

Widely accepted, serial numbered, highly reputable.

Choose a Gold IRA Company For Your 403(b) Rollover

Comparing the industry-leading 403(b) Gold IRA companies with the best reputations across the board. Focus on the User reviewed all of the leading companies so you can easily find one perfect for your 403(b) rollover to gold. It's important you review all companies, consider your options, and plan ahead.

403(b) Rollover FAQ

No, traditional 403(b) accounts do not allow direct investments in physical gold. You would need to roll it over into a self-directed IRA to hold physical gold.

A direct rollover from a 403(b) to a self-directed Gold IRA is tax-free. However, if funds are not transferred directly, they must be redeposited within 60 days to avoid taxes and penalties.

Documents generally include a rollover request form from your 403(b) plan provider and an account setup form for the new self-directed Gold IRA, along with proof of identification. Your chosen Gold IRA company will help you through everything you need.

Yes, but it depends on your 403(b) plan rules and your age. If you withdraw funds without rolling them over and you’re under 59½, penalties and taxes may apply.

You can invest in IRS-approved gold bullion coins and bars that meet fineness standards, such as American Gold Eagles and Canadian Gold Maple Leafs.

The process typically takes 2 to 4 weeks, depending on the efficiency of your Gold IRA company and the new custodian.

Your assets remain secure, as IRS-approved custodians are required to store them in third-party depositories. You would simply need to transfer the assets to a new custodian.

How Focus on the User Helps You Convert Your 403(b) to a Gold IRA

At Focus on the User, we provide clear resources to help you convert your 403(b) to a Gold IRA. With step-by-step guidance, you can plan ahead before you use your 403(b) funds to open a Gold IRA.